Automating Savings: How to Pay Yourself First

Automating Savings: How to Pay Yourself First

In today’s world of instant gratification and digital spending, saving money can feel like an uphill battle. With bills to pay, responsibilities to manage, and tempting purchases always a click away, setting aside money for the future often falls to the bottom of the priority list. But what if you could make saving effortless—something that happens automatically before you even get a chance to spend?

That’s the core idea behind automating your savings and the timeless financial strategy of “paying yourself first.” By prioritizing savings before expenses, and using automation to make the process seamless, you set yourself up for long-term financial health without relying on willpower alone.

Why Automating Savings Matters in Today’s Economy

Economic uncertainty, inflation, and rising costs make financial planning more important than ever. Yet despite these challenges, a 2023 survey by Bankrate found that nearly 57% of Americans wouldn’t be able to cover a $1,000 emergency with savings. This highlights a widespread issue: many people treat saving as an afterthought.

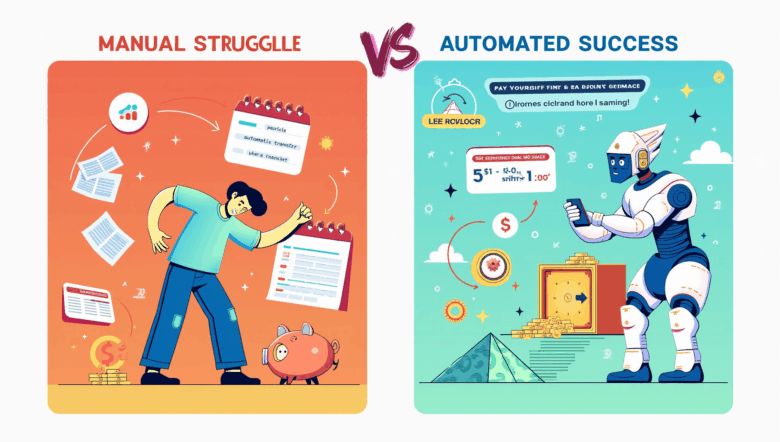

That’s where automation steps in. Instead of trying to remember to save or waiting to see what’s left at the end of the month, you build a system that does it for you—consistently and effortlessly.

What Does It Mean to “Pay Yourself First”?

Paying yourself first means you treat saving as a top financial priority—not something you do if there’s money left over. The idea is simple but powerful: when your paycheck arrives, the first thing you do is move a portion into savings or investments before spending on anything else.

Think of it as an investment in your future before anyone else’s—before landlords, utility companies, credit card issuers, or retailers get their cut.

Key Concepts Behind Automating Savings

1. Behavioral Finance Meets Technology

Humans are hardwired to favor instant rewards over future gains. Automation helps sidestep that tendency by removing decision-making from the process.

2. Consistency Beats Perfection

You don’t need to save hundreds every paycheck. Automating even small amounts regularly (like $25 a week) can lead to thousands saved over time, thanks to compound interest and habit formation.

3. Out of Sight, Out of Mind

Money moved automatically into a savings or investment account becomes less tempting to spend. This psychological barrier makes it easier to build a nest egg.

How to Automate Your Savings in 5 Simple Steps

Step 1: Set Clear, Specific Goals

Before automating savings, identify what you’re saving for. Clear goals keep you motivated and guide how much to save and where to save it.

-

Emergency fund: Aim for 3–6 months of living expenses

-

Vacation fund: Estimate the cost and target a completion date

-

Down payment: Set a timeline and budget for a home or car

-

Retirement: Use retirement calculators to estimate long-term needs

Example: Maya wants to take a $3,000 trip to Japan in 12 months. That means saving $250 per month. Automating this goal makes it achievable without last-minute scrambling.

Step 2: Choose the Right Accounts

Set up separate savings accounts for each goal to prevent confusion or accidental spending. Consider the following options:

-

High-yield savings accounts for emergency funds or short-term goals

-

Certificates of deposit (CDs) for medium-term goals with a fixed time horizon

-

Retirement accounts (401(k), IRA) for long-term goals

-

Investment accounts for wealth-building beyond your emergency fund

Tip: Nickname your accounts (e.g., “Dream Vacation Fund,” “Emergency Cushion”) to stay focused on the goal.

Step 3: Set Up Automatic Transfers

Work with your employer or bank to automate savings:

-

Direct deposit: Have a portion of your paycheck sent directly to your savings account. Many employers allow splitting your paycheck between accounts.

-

Bank transfers: Set up recurring transfers on payday from your checking account to your savings.

-

Apps and fintech tools: Use apps like Qapital, Acorns, or Digit that automate savings based on your spending habits or round up purchases.

Real-world scenario: Jordan sets a $100 auto-transfer every payday to his emergency fund. Over a year, that adds up to $2,600—without any manual effort.

Step 4: Align Transfers with Your Pay Schedule

Timing is everything. Schedule your savings transfer right after you receive your paycheck, so you don’t spend it before it gets moved.

-

Paid biweekly? Schedule biweekly transfers.

-

Freelance or irregular income? Set reminders or use percentage-based saving.

Pro Tip: Use the “bucket” strategy—automatically funnel money into different “buckets” like bills, savings, and spending as soon as income hits your account.

Step 5: Monitor and Adjust as Needed

Your budget and life will change. Periodically check on your savings goals and make adjustments:

-

Increase contributions after a raise

-

Reduce transfers temporarily if cash flow is tight

-

Reallocate savings when goals are reached

Use tools like personal finance dashboards or monthly review checklists to stay informed.

Advanced Strategies to Boost Automated Savings

1. Save Windfalls Automatically

Bonuses, tax refunds, or gifts can be set to deposit straight into savings. Treat unexpected money as an opportunity to accelerate your goals.

2. Incremental Increases

Use a “step-up” approach—every few months, increase your automated savings by a small percentage (e.g., 1–2%). You won’t feel the difference, but it adds up fast.

3. Use Employer Retirement Matching

If your employer offers 401(k) matching, contribute enough to get the full match—it’s essentially free money. Automate these contributions via payroll.

4. Round-Up Features

Banks and apps like Acorns round up purchases to the nearest dollar and invest the difference. It’s micro-saving, but it adds up over time.

Common Myths and Misconceptions

Myth 1: “I don’t make enough to automate savings.”

Truth: Start small—even $5 or $10 per week is better than nothing. The habit matters more than the amount.

Myth 2: “I’ll lose flexibility.”

Truth: Most automated transfers can be paused or adjusted at any time. You’re still in control.

Myth 3: “I’ll forget about my savings.”

Truth: That’s the point! Automating helps you save in the background while you focus on living your life.

Success Stories: Everyday Automation Wins

Alicia’s Wedding Fund

Alicia and her fiancé wanted a $15,000 wedding in 18 months. They automated $400 per month into a joint savings account. With discipline and automation, they reached their goal without taking on debt.

Dev’s Emergency Fund Journey

Dev had never saved consistently. He started with $25/week automated to a high-yield savings account. In one year, he had over $1,300 saved—enough to cover car repairs and medical bills without stress.

Final Thoughts: Make Your Future Self Proud

Automating your savings and paying yourself first is one of the most powerful habits you can develop for financial success. It turns good intentions into consistent action—without needing constant willpower or budgeting gymnastics.

Start today by setting a small, automated transfer aligned with a specific goal. Over time, you’ll not only build financial security but also peace of mind.

Remember, it’s not about how much you earn—it’s about how much you keep and what you do with it. Your future self will thank you.

Need help choosing a savings app or setting up automation? I can help you compare tools or design a savings plan—just ask!

Would you like this turned into a downloadable PDF, checklist, or email series? Let me know how else I can support you.