Short-Term vs. Long-Term Savings: What You Need to Know

Short-Term vs. Long-Term Savings: What You Need to Know

In today’s rapidly changing economic climate, saving money is more than just a good habit—it’s a necessity. Whether you’re saving for a rainy day or planning for retirement, understanding the distinction between short-term and long-term savings is crucial. Each serves a different purpose, has its own strategy, and requires a unique approach. Knowing how to balance both can set you on a path to financial stability and peace of mind.

In this article, we’ll explore the fundamentals of short-term and long-term savings, examine the benefits and challenges of each, and provide practical strategies to help you build a balanced savings plan that fits your life.

What Is Short-Term Savings?

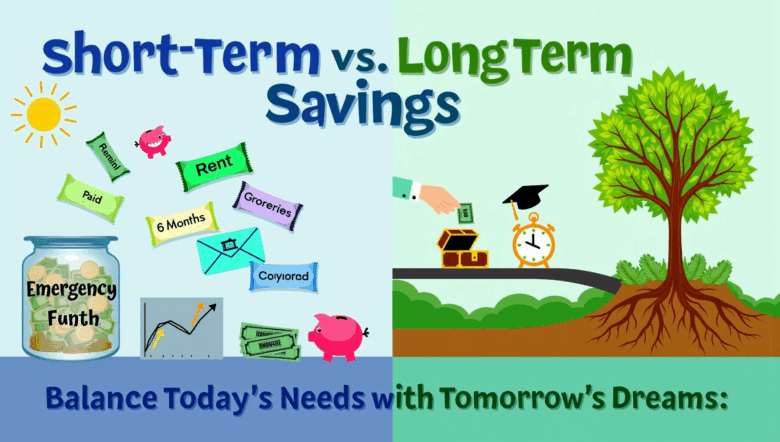

Short-term savings refers to money you set aside for goals or needs that will occur within the next one to three years. These savings are usually kept in easily accessible, low-risk accounts. The focus here is on liquidity and capital preservation rather than growth.

Common short-term savings goals include:

- Emergency fund (typically 3–6 months of living expenses)

- Vacation or travel

- Home repairs or maintenance

- Wedding expenses

- Holiday spending

Where to keep short-term savings:

- High-yield savings accounts

- Money market accounts

- Certificates of deposit (CDs) with short terms (under a year)

Key features:

- High liquidity

- Low risk

- Low to moderate interest returns

What Is Long-Term Savings?

Long-term savings is money set aside for goals that are five or more years away. These savings often focus on wealth accumulation, using interest, dividends, and compound growth over time.

Common long-term savings goals include:

- Retirement

- Buying a home (beyond a 3-year timeline)

- Children’s education

- Starting a business

Where to keep long-term savings:

- Retirement accounts (401(k), IRA, Roth IRA)

- Investment accounts (stocks, ETFs, mutual funds)

- Real estate or other appreciating assets

Key features:

- Lower liquidity

- Higher potential risk and reward

- Emphasis on long-term growth

Why the Distinction Matters

Understanding the difference between short- and long-term savings ensures you allocate your resources wisely and avoid financial shortfalls. If you place all your savings in long-term investments, you may struggle with liquidity in an emergency. On the other hand, if you only save for the short term, you might fall short of your long-term financial goals.

A balanced approach can help you weather financial storms while building a secure future.

Key Considerations When Planning Your Savings

1. Time Horizon

Your goal’s timeline will determine your savings strategy. Urgent or near-future goals require easy access to funds, while distant goals allow you to ride out market fluctuations.

Example: If you’re planning a wedding in 18 months, putting that money in stocks could expose you to unnecessary risk. A high-yield savings account is safer.

2. Risk Tolerance

How much volatility are you comfortable with? Long-term savings vehicles usually involve market risks, but they also offer the potential for greater returns.

Example: Retirement accounts may fluctuate in value, but historically, they yield higher returns over decades compared to savings accounts.

3. Liquidity Needs

Consider how quickly you need access to your money. Short-term savings should be liquid enough to withdraw without penalties or market loss.

Tip: Keep at least three months of expenses in a liquid emergency fund to protect yourself against job loss or unexpected bills.

4. Inflation Impact

Inflation erodes the purchasing power of money over time. Long-term savings should be in vehicles that can outpace inflation.

Example: Keeping retirement funds in a traditional savings account might preserve capital but lose value in real terms. Investing in diversified assets can help counteract inflation.

5. Tax Implications

Different accounts have different tax treatments. Tax-advantaged accounts like IRAs or 401(k)s offer benefits for long-term savers, while savings accounts may incur taxes on earned interest.

Practical Tips to Balance Both Types of Savings

1. Establish an Emergency Fund First

Before investing or saving for long-term goals, prioritize an emergency fund. This creates a financial buffer and prevents you from dipping into retirement savings prematurely.

2. Use Buckets or Goals-Based Budgeting

Set up separate accounts for each savings goal—short-term and long-term. Label them clearly (e.g., “Emergency Fund,” “Vacation 2025,” “Home Down Payment,” “Retirement”) to stay organized and motivated.

3. Automate Your Savings

Set up automatic transfers to your short- and long-term savings accounts. Automation reduces the temptation to spend and ensures consistency.

Tip: Even small amounts—like $25 a week—can add up significantly over time with consistent saving and compounding.

4. Revisit and Adjust Regularly

Life changes, and so should your savings strategy. Review your financial goals every 6–12 months and adjust contributions based on income, expenses, and shifting priorities.

5. Leverage Employer Benefits

If your employer offers a retirement savings match, take full advantage. It’s essentially free money and accelerates your long-term savings growth.

Example: If your employer matches 5% of your salary and you earn $50,000, that’s an extra $2,500 annually toward your future.

Real-Life Scenarios

Scenario 1: Newlyweds Planning Their Financial Future Emily and Jack just got married. They set up a short-term savings account for a honeymoon and an emergency fund. At the same time, they start contributing to their employer-sponsored 401(k) plans to build long-term wealth.

Scenario 2: The Mid-Career Professional Thomas, a 40-year-old engineer, has a healthy retirement portfolio but no liquid savings. A medical emergency forces him to sell investments at a loss. He learns the importance of maintaining both short-term and long-term savings.

Scenario 3: The College Graduate Riya just landed her first job. She opens a high-yield savings account for moving expenses and starts investing in a Roth IRA for retirement. With time on her side, her long-term investments have decades to grow.

Final Thoughts

Understanding the difference between short-term and long-term savings is essential to financial wellness. Each type of savings plays a distinct role in your overall plan: short-term savings offer security and flexibility, while long-term savings provide the foundation for future goals and financial independence.

A well-rounded savings strategy balances both, ensuring you’re prepared for today’s surprises and tomorrow’s dreams. Start by identifying your goals, choosing the right savings vehicles, and committing to consistent contributions.

Take action today—open that emergency fund, start that retirement account, and put your money to work in ways that support your life now and in the future. With intention and discipline, you can build a strong financial future, one step at a time.